Healthcare organizations are under intense financial pressure. Margins are tight. Labor costs are rising. Reimbursements remain unpredictable.

At the same time, many providers are quietly losing revenue through virtual credit card (VCC) payments. What appears to be a convenient reimbursement method often includes hidden processing fees that reduce net revenue.

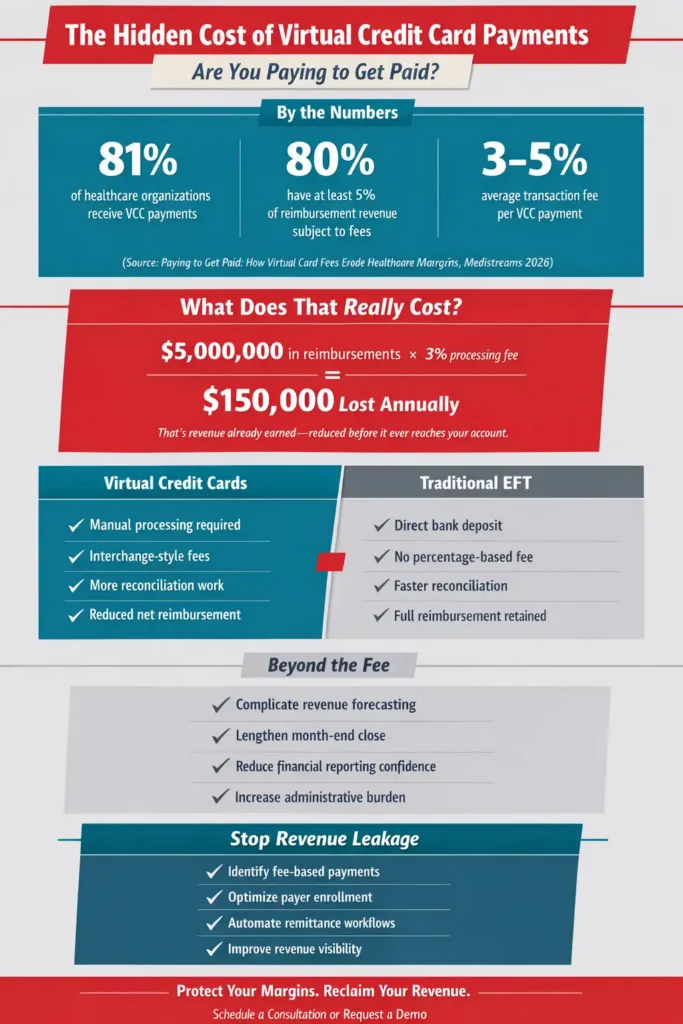

According to the 2026 report “Paying to Get Paid: How Virtual Card Fees Erode Healthcare Margins” by Medistreams, 81% of healthcare organizations have received reimbursements through virtual credit cards or similar programs. Additionally, 80% report that at least 5% of their reimbursement revenue is subject to fees, often ranging from 3% to 5% per transaction.

Over time, those percentages compound. As a result, thousands or even millions of dollars can disappear from operating budgets.

What Are Virtual Credit Card Payments in Healthcare?

Virtual credit cards were introduced as an electronic alternative to paper checks. Initially, they promised faster payments and improved security.

However, unlike traditional electronic funds transfer (EFT), VCC payments function like credit card transactions. Therefore, providers must manually process the payment and absorb interchange-style fees.

In simple terms, providers are paying to receive funds they already earned.

Why Are Virtual Credit Card Fees a Growing Problem?

How Much Revenue Is Lost to VCC Fees?

At first glance, a 3% fee may not seem significant. However, when applied across large reimbursement volumes, the financial impact grows quickly.

For example, if $5 million in reimbursements flows through VCC payments at 3%, the organization loses $150,000 annually.

Consequently, these fees reduce margins without improving patient outcomes or operational efficiency.

Here’s what virtual credit card fees can look like in real numbers:

Do Virtual Credit Cards Complicate Financial Operations?

Yes, and the impact extends beyond the transaction fee.

In addition to lowering reimbursement totals, VCC programs:

- Make net revenue forecasting more difficult

- Reduce confidence in financial reporting

- Lengthen month-end close cycles

- Increase manual reconciliation between deposits and remittances

Because fees are deducted before posting, reconciliation becomes more complex. As a result, accounting teams spend valuable time investigating discrepancies.

Why Are Providers Enrolled in VCC Programs Without Realizing It?

Surprisingly, many providers report being automatically enrolled in fee-based programs.

In many cases, payer communications are unclear. Meanwhile, opt-out processes may require manual outreach and repeated follow-up. Therefore, organizations often remain enrolled longer than intended.

Furthermore, limited visibility makes it difficult to measure the true financial impact until losses accumulate.

How Do Virtual Credit Cards Compare to EFT?

Although both methods are electronic, they differ significantly.

Traditional EFT:

- Deposits funds directly into a bank account

- Typically avoids percentage-based fees

- Supports easier reconciliation

Virtual credit cards:

- Require manual processing

- Include interchange-style fees

- Increase administrative workload

Unlike retail credit cards, VCCs do not reduce bad debt risk for providers. Yet they still impose transaction costs.

For additional guidance on electronic payment standards, review resources from the Centers for Medicare & Medicaid Services at https://www.cms.gov. Industry insights from the Healthcare Financial Management Association also emphasize stronger payment oversight (https://www.hfma.org).

How Can Healthcare Organizations Reduce Virtual Card Fees?

First, providers need visibility. Identify which payers are issuing VCC payments and calculate the total fees paid annually.

Next, evaluate payer enrollment preferences and opt out of fee-based payment programs when possible.

Finally, automation and revenue cycle expertise can simplify the process.

Virtual OfficeWare helps practices:

- Automate remittance handling

- Identify and flag fee-based payments

- Optimize payer enrollment

- Improve financial reporting transparency

As a result, providers retain more earned revenue while maintaining automation and steady cash flow.

For related revenue cycle insights, explore:

Stop Paying to Get Paid

Virtual credit card programs were designed to modernize payments. However, for many healthcare organizations, they have created hidden costs and operational strain.

Now more than ever, protecting every dollar of earned revenue is critical.

If your organization is unsure how much revenue is lost to VCC fees, now is the time to act.

Schedule a consultation or request a software demo to see how Virtual OfficeWare can help you reclaim revenue and strengthen your revenue cycle performance.